What Does House Poor Mean? This term refers to individuals who have stretched their finances to afford a home, leaving them with little to no disposable income for other essentials or luxuries. This blog will explore the question “What Does House Poor Mean?” and how this financial predicament affects daily living. By understanding “What Does House Poor Mean?” and its implications, you can make well-informed decisions to avoid this common financial trap.

Real estate investors Steve Daria and Joleigh emphasize the importance of a balanced budget when purchasing a home. They caution against overextending finances to secure a property, as this can lead to being house poor. Steve and Joleigh advocate for strategic financial planning to ensure homeowners don’t sacrifice their overall quality of life for homeownership.

What Does House Poor Mean?

What does house poor mean, exactly? At its essence, the term “house poor” encapsulates a scenario where individuals or families allocate a significant portion of their monthly income towards the various costs associated with homeownership.

These expenses typically include:

Mortgage Payments

Mortgage payments are a homeowner’s regular installments to reimburse the loan taken out to purchase the property.

These payments usually include both principal and interest, with the principal reducing the loan balance and the interest representing the cost of borrowing.

The monthly payment amount can vary based on the loan term, interest rate, and type of mortgage.

Property Taxes

Property taxes are annual levies local governments impose on real estate, calculated based on the property’s assessed value.

These taxes fund community services like schools, roads, and emergency services.

The amount can change widely depending on the property’s location and the local tax rate.

Insurance Premiums

Insurance premiums for homeowners insurance provide financial protection against potential damages to the property from events like fires, storms, theft, and other covered perils.

The cost of the premiums depends on the coverage amount, property value, location, and other risk factors.

Additionally, homeowners may need to pay for different types of insurance, such as flood insurance, depending on the area’s risk profile.

Maintenance Expenditures

Maintenance expenditures encompass the routine upkeep required to keep a property in good condition, including lawn care, HVAC servicing, and plumbing repairs.

Regular maintenance helps prevent more significant, costlier issues down the line and ensures the property remains safe and habitable.

These costs can be unpredictable and vary significantly based on the property’s age, size, and condition.

Utilities

Utilities include essential services such as electricity, water, gas, and garbage collection for a home’s functioning and comfort.

These monthly expenses can fluctuate based on usage, the size of the property, and seasonal changes.

Homeowners must budget for these recurring costs to ensure their homes remain livable and efficient.

Get An Offer Today, Sell In A Matter Of Days…

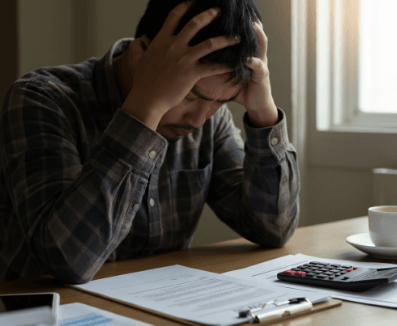

The Symptoms of Being House Poor

When you’re house-poor, most of your income is swallowed by mortgage payments, property taxes, maintenance, and utilities, leaving little for other expenses.

This precarious financial state can lead to stress and a lack of funds for emergencies or leisure. Symptoms of being house-poor include:

High Debt-to-Income Ratio

Much of your income goes towards your mortgage and other housing-related expenses, leaving little for other necessities or savings.

Limited Cash Flow

After covering housing costs, more money is often needed for savings, investments, or discretionary spending.

This can prevent individuals from building a financial cushion or investing in their future.

Stress and Anxiety Over Finances

Worrying about making ends meet each month becomes a regular part of life, leading to increased stress and anxiety.

This financial strain can impact overall well-being and quality of life.

How Does One End Up House Poor?

Several factors contribute to this precarious financial position:

Overbuying

Purchasing a home that’s too expensive for your budget can quickly lead to being house-poor.

For example, buying a property that consumes more than 30% of your income can strain your finances significantly.

Unanticipated Expenses

Only underestimating the costs associated with homeownership, such as repairs, maintenance, and upgrades, can lead to unexpected financial burdens.

For instance, an unforeseen roof repair or primary appliance replacement can significantly strain your budget.

Income Changes

Reducing household income due to job attrition, illness, or other unpredictable circumstances can make it difficult to meet mortgage payments and other housing costs.

Even temporary income disruptions can have long-term financial consequences.

Strategies to Avoid Becoming House Poor

It is crucial to navigate the tricky waters of homeownership without falling into the trap of becoming house-poor.

Below, we’ll explore practical strategies to help prospective and current homeowners maintain financial balance and security.

Understand the Full Cost of Homeownership

Beyond the mortgage, factor in all related expenses before buying.

This includes property taxes, insurance, maintenance, and utilities.

For example, create a detailed budget that accounts for all these costs to understand the genuine financial commitment.

Stick to a Budget

Know what you can afford and resist the temptation to stretch your budget for a more expensive property.

Use tools like mortgage calculators to determine how much you can realistically afford without compromising other financial goals.

Build a Safety Net

An emergency fund typically equals 3-6 months of current expenses, including your mortgage.

It can buffer against unexpected financial challenges and help cover costs for job loss or significant repairs.

Consider Future Income Stability

Be realistic about your future earnings potential and the security of your income sources.

Assessing job stability and potential career growth can help you sustain homeownership costs in the long term.

Managing If You’re Already House Poor

If you find yourself in a situation where the meaning of “house poor” has become a reality, there are things you can take to improve your circumstances:

Refinance Your Mortgage

Look into refinancing options to lower your monthly payment.

Refinancing to a lessened interest rate or extending the loan term can reduce your financial burden.

Cut Unnecessary Expenses

Review your spending habits and cut back where possible.

This might include reducing discretionary spending, canceling subscriptions, or finding cost-effective alternatives for necessary expenses.

Increase Your Income

Seek raises, promotions, or side gig opportunities.

Additional income streams can provide financial relief and help you build a buffer against future economic challenges.

Downsize

If other measures don’t relieve the pressure, consider moving to a less expensive home.

Downsizing can reduce your mortgage payment and other housing costs, freeing up income for different needs.

Conclusion

Understanding “What does house poor mean?” is an exemplary tale for anyone looking to buy a home. It underscores the importance of purchasing within your means, understanding the full scope of homeownership costs, and preparing for the unexpected. By adopting prudent financial planning and budgeting strategies, aspiring homeowners can avoid the pitfalls of becoming house-poor and enjoy the many benefits of homeownership.

By understanding what does house poor mean and implementing strategies to prevent it, homeowners and potential buyers can make knowledgeable decisions that lead to financial stability and peace of mind.

**NOTICE: Please note that the content presented in this post is intended solely for informational and educational purposes. It should not be construed as legal or financial advice or relied upon as a replacement for consultation with a qualified attorney or CPA. For specific guidance on legal or financial matters, readers are encouraged to seek professional assistance from an attorney, CPA, or other appropriate professional regarding the subject matter.